51

Notes to Financial Statements

December 31, 2014

2. Summary of Significant Accounting Policies (cont’d)

ADOPTION OF NEW AND REVISED STANDARDS (cont’d)

FRS 115 Revenue From Contracts with Customers

In November 2014, FRS 115 was issued which establishes a single comprehensive model for entities to use in

accounting for revenue arising from contracts with customers. FRS 115 will supersede the current revenue

recognition guidance including FRS 18 Revenue, FRS 11 Construction Contracts and the related Interpretations

when it becomes effective.

The core principle of FRS 115 is that an entity should recognise revenue to depict the transfer of promised goods

or services to customers in an amount that reflects the consideration to which the entity expects to be entitled

in exchange for those goods or services. Specifically, the Standard introduces a 5-step approach to revenue

recognition:

• Step 1: Identify the contract (s) with a customer.

• Step 2: Identify the performance obligations in the contract.

• Step 3: Determine the transaction price.

• Step 4: Allocate the transaction price to the performance obligations in the contract.

• Step 5: Recognise revenue when (or as) the entity satisfies a performance obligation.

Under FRS 115, an entity recognises revenue when (or as) a performance obligation is satisfied, i.e. when “control”

of the goods or services underlying the particular performance obligation is transferred to the customer. More

prescriptive guidance has been added in FRS 115 to deal with specific scenarios. Furthermore, extensive disclosures

are required by FRS 115.

Management is currently evaluating the potential impact of the application of FRS 115 on the financial statements

of the Group and the Co-operative in the period of initial application.

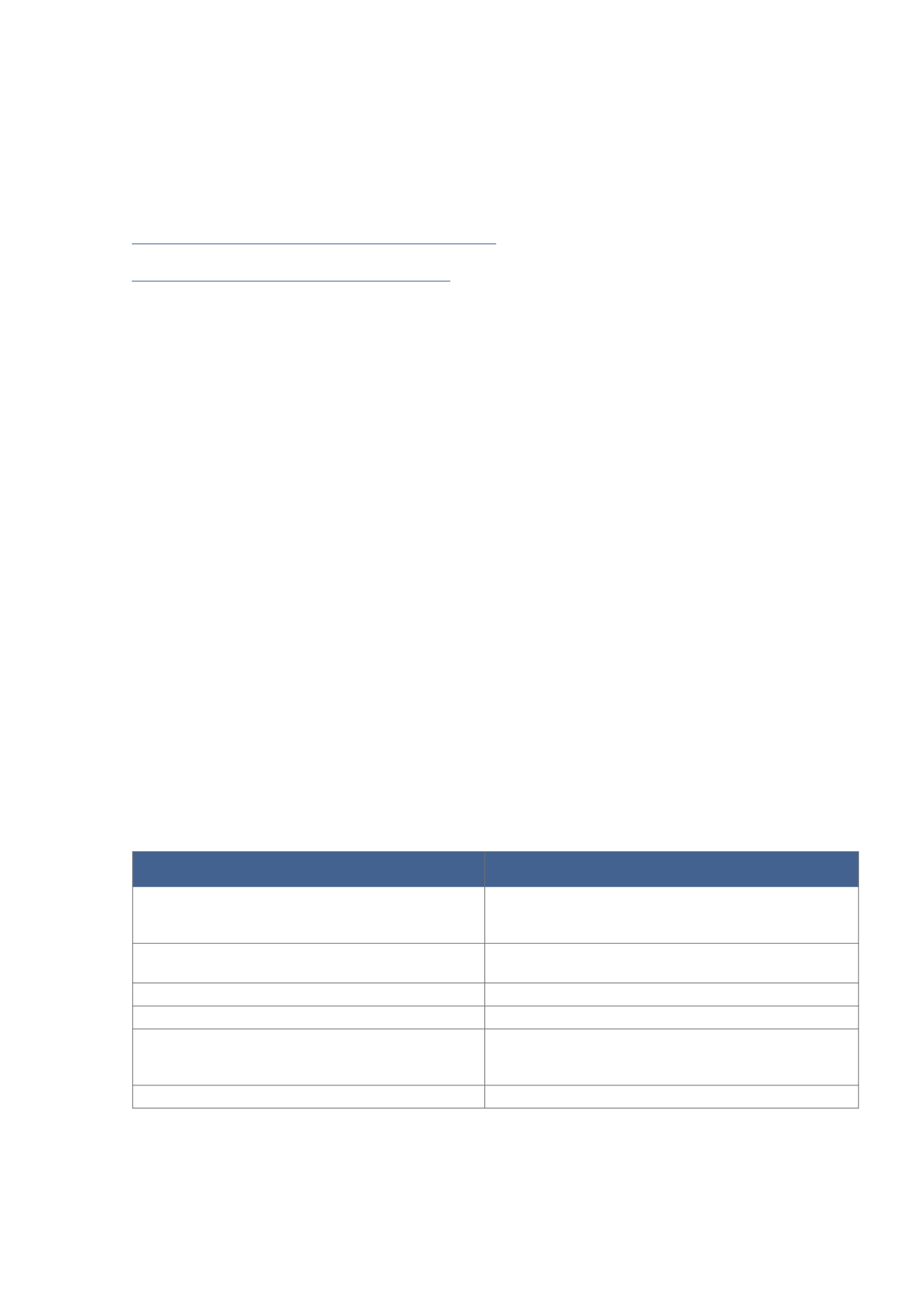

The following table shows the topics addressed by the

Improvements to Financial Reporting Standards

:

Management is currently evaluating the potenial impact of the application of the above Improvements to Financial

Reporting Standards on the financial statements of the Group and the Co-operative in the period of initial application.

FRS

Subject of amendment

FRS 103

Business Combinations

Accounting for contingent consideration in a business

combination

Scope exceptions for joint ventures.

FRS 16

Property, Plant and Equipment

Revaluation method—proportionate restatement of

accumulated depreciation

FRS 24

Related Party Disclosures

Key management personnel

FRS 113

Fair Value Measurement

Scope of paragraph 52 (portfolio exception).

FRS 40

Investment Property

Clarifying the interrelationship between FRS 103 and FRS

40 when classifying property as investment property or

owner-occupied property

FRS 107

Financial Instruments: Disclosures

Servicing contracts.